Bulletin – Debt

27th May 2020

| Debt and The Pandemic Article by Patrick McIntosh, [email protected] |

Creating the money. Where does it go and how do we pay for it? What is KMG’s position with our investment strategies?

‘’The process by which money is created is so simple that the mind is repelled” so said JK Galbraith.

History

There is nothing new about pandemics any more than there is anything new about paying the cost of sorting out the mess that rogue viruses create.

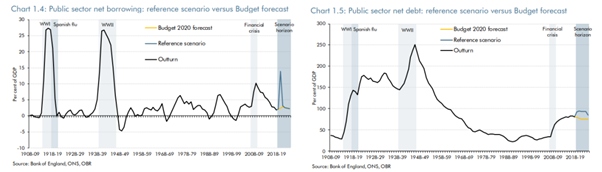

Wars and pandemics have one thing in common: they cost an awful lot of money, they destroy huge amounts of wealth, they eat up many innocent lives and the consequences are felt by many generations to come. As a good example, we should not forget that we only recently cleared the Napoleonic and World War debt, and the graphs below show how the debt has been cleared over decades. The same will be true again from the current pandemic.

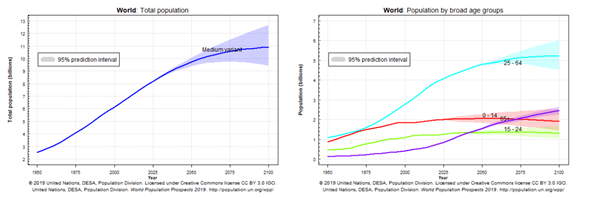

If there is one difference today by comparison with any of the previous debt binges it is that the human demographic is now, for the first time, levelling off and the world is potentially moving towards shrinking both its population and material wealth. The UN graphs below show how this phenomenon is likely to play out.

Money Creation

For 6,000 years or more governments have given permission to bankers to create money out of nothing. They have licensed them on the basis that the bankers have sufficient intelligence to understand the relationship between the money they create and lend based on the ability of the borrower to be able to repay both the principal and interest.

As we all know, money is a confidence trick, and in its simplest form a “run on the bank” as portrayed in Mary Poppins, demonstrates how fragile that confidence can become. More recently those people who queued around the block when Northern Rock went bust in 2008/9 will remember all too clearly how quickly confidence in the banking system can be destroyed if they feel politicians have mislead us by printing money beyond reasonable reality.

Whether you are a Marxist, a monetarist, or a Keynesian economics believer, there is one thing that all have in common: when you create money, and you put it to work, the wealth it creates in greater employment, larger economic activity and expanding global wealth enable the banker and the government to extract interest and taxation. This not only services the immediate requirements of the debt, but ultimately pays back the debt as well as the interest in a reasonable period.

Is it different this time?

There are various reasons why the following three paragraphs may be challenged in the future because of the way in which the globe and its population are now evolving. However:-

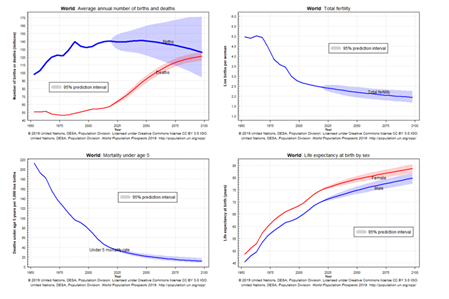

- As we have pointed out many times recently the number of babies being born in the world has not changed for more than 20 years (see charts on this point below). The only reason the population of the world has expanded is because average lifetimes have got longer. Therefore, the future becomes significantly challenging as the ageing population comes to an end. The best example of this in real time is to look at what is happening in Japan where their debt is more than twice our own and advancing in the pandemic ahead of us.

- In Europe, the proportion of the population of working age has been in decline. (The share of people aged 80 years or more should more than double by 2100 to nearly 15% of the whole population). This has been arrested by inward migration, but the decline is set to continue into the foreseeable future – as with Japan and other maturing affluent societies.

- An ageing population, which sadly of course is now being interrupted by the pandemic, creates enormous strains upon all economies who have promised, but not funded for, welfare benefits in the form of pensions, healthcare etc. These had already become challenging to the global economy before the pandemic with a debt that had been created to help society through the ageing crisis well before the pandemic started.

The above three key points are absolute facts and really cannot be disputed by anybody. They will play a significant part in the whole management of the debt that we currently entertain. The uncertain and subjective dilemma relates to global and individual wealth (there is evidence that we are possibly moving away from demonstrative material wealth) and how we feel and judge ourselves in terms of wealth amongst our peer group and not just our desire for material assets in a post-COVID world.

There is clear evidence in everything we do and everywhere we look that technology is transforming and improving our intellectual wealth, the way in which we live our lives and our perceived need for material wealth. If there is one thing that global government and bankers have found impossible to master or control is how you extract repayment from changing consumption patterns, when there is no material evidence upon which a demand can be made. How do you tax a free YouTube download? In principle, governments could still impose a fixed tax on downloads, e.g. 5 pence a time, or tax YouTube itself, and this requires a radical change from the past.

A simple example of this phenomenon was heard on the radio recently where a performer observed that despite the fact that her musical creations have been downloaded millions of times across the world, she had actually only received remuneration of a few pence. We have all enjoyed lockdown in different ways. One thing that we have all taken advantage of is the plethora of extremely cheap entertainment on the radio, the television, our tablets and our telephones for which we have either paid an extremely small amount of money or nothing at all for the privilege of this extraordinary high-quality entertainment. Just think about not going to the cinema: no expenses to get there, no tax on fuel or payment for transport, no ticket purchase, no treats when there; all loss of tax to government.

Unemployment

One of the many unfortunate consequences of the pandemic is the probability of significant increases in unemployment. This causes a reduction in working people paying taxes or contributing to interest on monies borrowed, as well as more claiming universal credit (from the benefit system), thus creating a drain on the Exchequer. From entertainment to travel, working in an office to travelling on public transport, many many of the traditional ways in which money in circulation has enabled banks and governments to extract a small amount of payment from each and every one of us is greatly reducing. Those individual contributions to the wealth and repayment of society may now be in short supply both in the short term, but possibly in the longer term, especially if we are to work from home where we do not need public transport or coffee shops, sandwich bars etc.

The question is this: will alternative economic activity be sufficiently robust to pick up the lost revenue from actions we may no longer take in living our lives?

Taxation

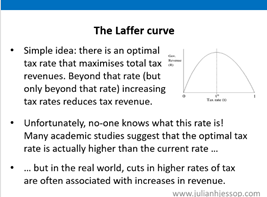

There is an interesting principle which remains constant throughout history and has more recently been coined the “LAFFER CURVE”. What this has shown is that there is a maximum amount of taxation extraction that you can take from society in the form of interest or taxation to meet your spending or debt repayment requirements.

We must expect in the outcome of this pandemic that there will be a redistribution of the way in which society pays for, or services, the benefits that we all need to survive in a modern social economy. As the overall amount of money that all governments around the world can collect from their populations will not increase significantly, it is undoubtedly a fact that the more wealthy individuals and prosperous companies will share more of the burden in servicing the costs of the debt to provide the benefits that we have promised our ageing population.

The Big Issue

But here is the big elephant in the room: the elephant is significantly larger than the room! Extreme adoption of the usual arrangements (as detailed later in this report) will have to be made to manage the current debt crisis through preceding generations, especially if the global population continues to age and possibly shrink.

When there are fewer working people and we have extraordinary advances in technology, (entertainment and experience streaming), then we all become better off. If, as seems possible, we need less and less, there will be less money in circulation and if there is less money in circulation there is less ability to pay interest, there is less ability to tax and so there then becomes less ability to fund healthcare, pensions, infrastructure, interest and debt reduction.

So, without making any judgements or calls on the means by which we manage our way out of the pandemic, we remind you to consider that any or all of the following fundamental actions of governments may apply into the future:

Inflation

To quote Milton Friedman: “Inflation is always and everywhere a monetary phenomenon”.

Inflation has and always will be a means by which debt can be reduced, as is proven by Consols (a form of government debt) which were raised from the Napoleonic Wars or War Loans from the First and Second World Wars. These had real value when issued to patriotic public keen to support the war effort at the time. Yet those same investors lost value through inflation which came to the rescue of governments around the world.

Some have argued that inflation is now impossible because of a shrinking global population; but it must be remembered that in the 1970’s and 80’s when we had millions of unemployed and a collapsed economy, we had 25% inflation and we had a huge wage demand. To some large extent the debt leftover from the previous global wars and pandemics was a consequence that we never really addressed. The world lost confidence in the value of money, and Britain almost went bust (lest we forget).

It is not at all impossible for governments around the world to engage in financial engineering, whereby interest rates are maintained at artificially low levels while inflation is allowed to reach much higher levels, as a means of reducing the amount of debt.

If we are to have inflation, then maintaining and investing in property and equity is a good idea. Borrowing money is an excellent idea, as many of our clients enjoyed in the 70’s and 80’s but owning debt or investing in cash is a very bad idea.

Fill your boots with very cheap debt forever

An option that appears to be increasingly popular across the world, and is well demonstrated in Japan, is that while interest rates are ridiculously low governments borrow as much as they can (this was Corbyn’s idea in the last election and now being happily followed by Sunak). Indeed, as we prepare this article, we note in the Financial Times that the UK government has just issued debt with a negative interest rate! This means that the Government is borrowing say £100 and only offering to pay back £99 – that is the sense in which the ‘interest rate’ (the yield to maturity) is negative.

Let us assume that you can charge a nominal rate of interest. We know that the base interest rate in the UK is 0.1%. Therefore, £300 billion of debt costs £300 million in interest. If you decide to borrow the money for 100 years without ever paying it back that really is not a very great demand on the UK Exchequer for several generations to come. By the time the debt must be repaid we will all be dead, as will our children and probably most of our grandchildren!

Paying for it

We have mentioned taxation above in relation to the Laffer Curve, but here is another significant observation:

Taxation will change, and the better off will pay a higher proportion of their wealth towards debt.

But the absolute reality in this case is the absolute fact that there are fewer people available in the developed economies of the world who are in work and who are creating income upon which tax can be collected. At the same time, many people are beginning to move away from owning so many assets like property, cars, boats, antiques paintings, and other fixed assets that can be taxed as some form of wealth tax. We are moving much more towards a rented society: rented holidays, rented music and rented entertainment, and it is the inevitable fact of an evolving technological lifestyle that we are all adopting and enjoying a less permanent lifestyle. People wish for more flexible opportunities to live experiences without commitments. This rented lifestyle requires a very different way of taxation. This may lead to much more sophisticated consumer taxation e.g. VAT at 25% on holidays and 5% on food.

Increased Wealth

Governments and bankers may achieve some equilibrium between the amount of money raised and the ability to service the debt from a significant improvement in the wealth of us all. Higher quality public services and public transport mean higher wages and higher prices. All of these evolving events will mean that there will be higher levels of revenue that can come back to banks and thus consumption taxes can be raised back to governments as time goes by.

If the money created now is spent sensibly on infrastructure improvements and general wealth creation, then there is a reasonable possibility of some form of balanced budget into the future. This in turn should help to balance the books over the longer term. And if you can borrow money over a long period at very low rates of interest, who cares?

To give this a domestic slant think about how parents view mortgages against education for the children. People may choose to borrow money against the house in order to have a good quality of life in bringing up the family and providing a good environment for the family in a good home rather than live much more modest lives in more modest accommodation. In other words, mortgaging the future for the benefits of the family today. We all make trade-offs between the here and now, the future and our natural desire to invest for a better life for ourselves and our children, and from a country perspective, government also make much the same decisions

Moral Hazard

What society around the world has got to decide is at what point we agree that it is okay to magic money out of nowhere without worrying about the consequences for the future.

Conclusions

The mountains of debt that are now being created (and there is much more to come) will be managed into the future through a combination of the ideas shared in this paper.

The debt will not be insurmountable. As we have always done in the past, over time, we will absorb the debt into our new normal way of life.

One part of the solution may be that as the world forgave debt to the Third World not so long ago, there will be some gerrymandering amongst so-called affluent western economies who will find convenient ways of cancelling some of the debt generated through the pandemic.

Another part of the solution will be taxation which will change, and for some will go up, but on average the amount of taxation collected from the population may remain reasonably constant. We suspect there will be a greater burden of taxation placed on wealthier companies and individuals.

Inflation is likely to be higher in the future than it has been in the recent past, even if it is artificially manipulated to achieve the outcome.

We will keep the illusion and confidence trick of money going for everybody. The debt may become 2, 3, 4 or even 5 times greater than it is today. If we do not do this, the social dislocation, the hardship and poverty, and the inevitable collapse in global civilisation may be upon us faster than we can possibly cope with.

What is KMG doing about all this?

In recognition of these key points which we constantly review in our Investment Committee meetings we will make sure that we reflect these competing issues in maintaining a balanced investment strategy,

KMG has no political or ideological position on any economic theory. We will not bet on any particular outcome, but will continue to diversify and minimise risk by assuming all or any one of these arrangements (along with a whole host of others that we could have bought into this paper) may come to pass as the pandemic evolves and passes, and another threat to the future global economy inevitably develops.