Bulletin – Syndemic v Pandemic

29th October 2020

| Article by Patrick McIntosh, [email protected] |

The Investment Committee met on 27th October 2020 to review the state of play and the positive position we have achieved for all our clients in the face of a very challenging investment environment.

The good news …

In addition to achieving positive investment returns this year and over the last 12 months with your investment portfolios out-performing the FTSE 100 index by more than 20%, the Financial Times announced last week that KMG is one of Britain’s top 100 financial advisors! We will be sending out more information on this accolade soon but fundamentally it is about quality of advice, level of service, performance of investment return and the whole panoply of financial advice which is so important to you all. We feel very proud to be in this unique and select group.

Syndemic v Pandemic

There was a great deal on the agenda for the Investment Committee this month, not least of course the up-coming US presidential election and the possibility of not only the President but also the Senate moving from Republican to Democrat and whether this would have much effect on the global economy? We think not, as markets have largely discounted all possible outcomes and, in reality, politicians are completely at the mercy of the evolution of the pandemic for the next 12 to 18 months.

Brexit rumbles on but how relevant in the post-pandemic world are any of the arguments raised before March 2020? By example, in the UK and in the USA the issue of migration has evaporated as an election issue, and yet these were burning issues in both the US election four years ago and around the Brexit debate at the same time. Fundamentally however the world remains fixated on the pandemic and both its current and long-term influences on society everywhere.

So, what is Syndemic?

Syndemic is the word used to consider the unintended consequences and outcomes of humanity’s actions in dealing with the pandemic. This includes the following:

- reporting other illnesses

- going for cancer screening and tests

- managing on-going illnesses and conditions such as diabetes

- the scarring effect on children in their developmental needs, social interaction, educational requirements, and personal development skills

- mental illness and the stress of coping with the world which seems to have no coherent structure or leadership helping us through these very challenging times

- people living at work, by which we mean the lack of distinction between work and leisure time. This in turn is likely to lead to enormous social and domestic pressure and dilemmas

- a lack of social integration. This means we are not being exposed to the normal illnesses that travel through society year by year and which automatically build up our general immunity. When we do return to social interaction do not be surprised by a significant uptick in all sorts of illnesses as we rebuild our general immunity.

All these factors continue to have considerable unknown outcomes and consequences for the global economy, the stability of society and harmonious global endeavour.

We conclude this section by observing that even though vaccines are developing pretty rapidly, full-scale immunisation and reasonable global herd immunity is probably some 12 to 18 months away, and until this is achieved economic performance will remain erratic. At the same time, the magnificent expansion of money supply created through fiscal stimulus and monetary expansion from central banks will help us all through the pandemic but will then leave a significant debt-legacy for generations to come… unless, as we suspect, the following three things happen:

- Pent-up demand which, once released, we believe could be extraordinary especially when combined with:

- the development of technical skills in artificial intelligence

- the adoption of technology in a myriad of other industries

- the massive investment that the world is about to make in re-skilling

- infrastructure spending, especially around decarbonisation

It is predicted that the global economy will expand by $1.5 trillion as the result of development in virtual reality (VR) and artificial reality (AR) which will revolutionise productivity, improve medical care, expand engineering skills, and develop rapid educational advancement in all ages. VR and AR will also lead to a complete revolution in entertainment in just about all its forms whilst at the same time expanding our ability to travel, enjoy, relax and improve our well-being. We are collecting anecdotal evidence from many clients across all sorts of industries who are already noticing these effects and subsequent opportunities.

- Much of the debt being generated will be written-off or considered as a grant. As the money now being borrowed is at such trivial interest rates it really does not matter whether we pay the money back to the central banks this century, next century or in any century! The cost of servicing the debt is almost irrelevant and will become increasingly so as other interest rates normalise and economies start to expand. In the proverbial observation of “kicking the can down the road”, this can is being kicked out of the stadium and probably into orbit and off to the moon and beyond.

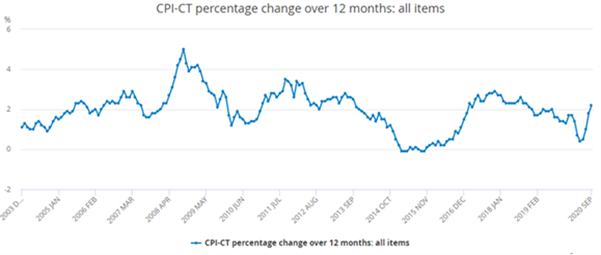

- Whilst it appears that we are living in a deflationary age with negative interest rates in five or six countries in Europe alone, inflation as Milton Friedman observed “is always and everywhere a monetary phenomenon”. And so, it is today: see the latest inflationary graph below:

The graph shows that inflation, excluding short term Government action on Eat out to Help out and reduced VAT, has suddenly risen to 2%. We would not be at all surprised if this rises to 5% in the next year and beyond, but why should this be?

Many factors may influence inflation. At the moment we are seeing higher house prices and at the same time we are seeing a move towards higher quality of life, spending more on better food and energy efficiency. The basic price of a haircut or any service-led industry has risen as the costs of the pandemic filter through to the end-user.

Do not be surprised to see an increase in the minimum wage and development of universal basic income in some form or other to help the less well off; and remember that this money will go into the system and drive up demand. Prices of raw materials are increasing, supply chains are changing and becoming very demanding whether it be importing raw materials such as iron, cement, lithium or even less-essential items such as clothes.

Inflation in Britain may also be exacerbated by Brexit and the possible challenges of an export/import system which may not be ready to cope with the rigours of independence from the EU. And we have not yet agreed enough alternative trade deals with other partners, although the Japanese agreement this month may be a template towards the future.

China

We remain challenged by China’s overall objective and observed in our Investment Committee meeting that it is extraordinary how the authoritarian Chinese government has managed to control society way beyond our ability in the West, and thus keep the pandemic under considerable control. The Chinese economy is expanding and developing. So, should we be worried?

China has taken advantage of global distraction around the pandemic and have also used the weakness of the American and European political situation to further their global ambitions. They will continue to re-assert themselves as the largest global economy. Remember that China’s history timeline is significantly longer than our own. The last 250 years where China has not been the largest economy in the world is a relatively short space of time in relation to their previous continuous period of global domination of thousands of years.

China desires to be a functioning global economy into which they can trade and prosper. It is not in their interests to destroy opportunities for global trade and wealth creation, and therefore as China matures into a dominant force so the rest of the world will re-shape their relationships with China into a robust but equally sound and positive way. So long as we are alive to these threats and we can meet them robustly we will benefit from China’s integration into an expanding global economy.

Taxation

The Committee’s conclusion on changing taxation is as follows:

Many things will happen in the future post Brexit, post the US election and when the pandemic appears to be under control. On the table this week was an OECD report recommending a global taxation on multi-national companies wherever they trade and wherever their profits are posted, but for now we expect that little will be done to change taxation as this would just be a step too far for humanity to contemplate and cope with.

Positive outcomes to help you through negative short-term concerns

As we have observed through this year, what we are experiencing is quite extraordinary. What we thought would happen over 10 to 15 years is happening over 10 to 15 months.

The outcome is going to be unbelievably beneficial to humanity:

- People will be better educated and have greater skill-sets

- Decarbonisation will accelerate, bringing wonderful opportunities for new employment and cleaner lives

- Medical science will be transformational, helped by the experience of the pandemic and the development of technology, especially in artificial and virtual reality

- Social cohesion will come together beyond our wildest imagination as we all learn that we have to live together and support each other, having learned that selfishness during a pandemic leads to untold misery for huge numbers of people.

The world has no choice but to work together to raise the money needed to get us through the pandemic and to support better democracy, less protectionism and greater personal ownership of responsibility. These things will provide huge investment opportunities incorporating Environmental, Social and Governance criteria (ESG in case you wondered what these letters stood for!) In turn this will help KMG to develop investment portfolios that not only produce good results for you but also beneficial outcomes for the planet and for humanity. It will be a win-win.

In the meantime, try to remain positive. Try not to get too involved in the noise of the immediate issues. Think to the future and remember that what you are doing to help yourself is also what the majority of the world’s population are also doing to move towards a post-pandemic and much brighter planet.

Living with risk

Perhaps the biggest challenges in society today involves reappraising our approach to risk and understanding that our individual approach to risk has profound effects upon how we view our investment portfolios, what we expect from our investment returns, and how we cope with volatility in a very uncertain world.

The pandemic has demonstrated to everybody that humanity is never immune from the effects of risk. We live with a whole range of uncertainty and yet, unfortunately, governments around the world have tried to convince the electorate that they have the magic ability to immunise everybody from these effects.

In the great financial crisis of 2008/9, we could have allowed banks to go bust. This would have demonstrated to humanity that all investments have risk attached to them, even cash! Unfortunately, in bailing out the financial system 10 years ago we not only piled more debt upon the global taxpayer, but we also pretended that we were immune from the risks created by human foibles and misunderstandings.

Education, and the lack of it, especially in the Western world has caused a problem of misunderstanding. We misunderstand risk itself, and we also misunderstand our responsibility in accepting daily risks. For example, in deciding who and what and how and when and which criteria to use in assessing our lives in every aspect of living. Restricting children’s ability to play and especially their ability to socially interact is now exacerbating the loss of the basic learning of risk.

And for grown-ups, adverts claiming to kill all known bacteria combined with the extraordinary addiction that humanity has in the developed world to the over-use of detergents is not only destroying the planet, but also doing little to enable each of us to accept that our human body has a much greater ability to self-immunise through exposure to infection, bacteria and the normal process of life.

The Investment Committee spends an enormous amount of time considering risk in all its forms from an economic, political, and fundamentally also from a human behavioural perspective. If there is one strength we think KMG clients particularly enjoy it is their knowledge of the investment risk profile, as well as the understanding of why we diversify our investment approach so widely and why we remain continuously sceptical about any investment fad that comes along.

However, we suggest that the pandemic has probably done more to force everybody to reappraise their approach to risk in all its forms and to accept that there is no magic government that can protect us all. The only way we can protect each and every one of us is to take much more responsibility for the ownership of our day-to-day lives as well as in our interaction with the rest of humanity and the planet.

Humanity started life as a single cell and has developed into the extraordinary human beings we are today. But who is to say that we have any more right to live on this planet than COVID-19, or any other bacterial evolution? COVID-19 teaches us that we are very close to the beginning of life, and to the end of life, and we should be far more respectful of our planet that is infinitely more powerful than any government or human can ever be.