Bulletin – Changes to what we value

21st December 2020

In a year of momentous social and medical drama it is perhaps the view of a different future that offers the most hope in the run-up to the end of 2020.

The re-opening of society has progressed as we expected at outset in terms of a series of waves, opening and closing of facilities, rising death rates and so forth. Despite the early prediction that January could see a further unpleasant wave of illness, I ask what will the reopening of society look like when it does inevitably happen? How many of the changes forced on us will stick, and what new forms of consumerism will be adopted?

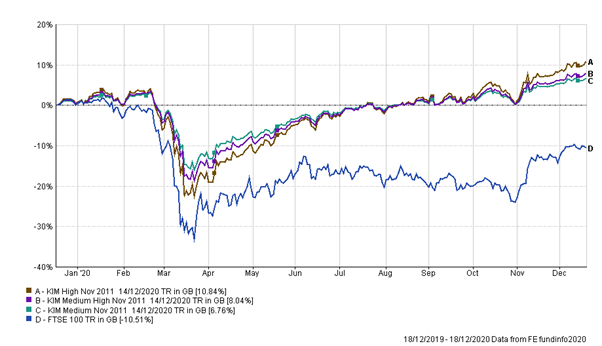

First however, it is worth again reflecting on how impressively the investment portfolios have performed through the year, despite holding a significant amount of cash just in case things worked out differently:

If adversity breeds invention, then what better time to see human ingenuity? The largely cooperative medical race, right across the Globe, showing just what is possible if clever people, money, and regulators work together – and the ripples will be wider than COVID alone.

COVID and its vaccine remain the most acute issues for society today, but the changes will be much broader and longer lasting in a variety of ways; and the longer we remain restricted in our behaviour, the more permanent these will become.

Across this future landscape we will find a common thread in that what we value, search for or demand instructs the way markets and governments act. Greater alignment with the world and its finite resources and the resulting financial opportunity will come in three hugely significant areas:

- Social change

- Climate action

- Infrastructure changes and opportunities

Amazon is the world’s most valuable company by market value today. We clearly value the service and goods it provides, (material and pointless though many of them are) and overlook the amount of pollution and plastic as a result of their transport around the world. We value the ease of access and the quick delivery. So, we value these more than the negatives of pollution, waste, and climate damage. Perhaps now is a turning point?

With fewer hours spent commuting, we have reclaimed time. We all applauded key workers earlier in the year, and yet what financial value do we put on the care provided in now-closed nursing homes? In the latter case, value is not linked to profit. Is now the time to reassess our values?

Environmental issues are with us like it or not, and correspondingly there is demand for unbelievably huge sums to be invested in this sector. For example: the enormous investment in infrastructure to decarbonise the National Grid and its constituent parts, growth in the market for electric cars, a doubling of electricity used in the UK by the middle of the century, and biodegradable replacements for plastic containers down to coffee cups and sandwich packaging. Ultimately it will be consumer demand and impatience that applies commercial pressure to industry.

Circular economies

The Friedman-style approach of profit being the goal at all cost has been central for the past 50 years, but the pendulum is moving back towards balance and thus the financially rewarding investments will begin to come from those deemed “worthy” post-COVID. In a world of finite resources, the principles of a more circular economy are important and desirable.

In other words, I think we should be prepared for a different and potentially more inflationary future, where the potential for valuable investments can be both profitable and less damaging to the planet.

The issues of the day

With so much going on in the world, I have provided some brief thoughts on the key issues facing us in the immediate future:-

The Vaccine

While COVID-19 may never be defeated – indeed the idea or image that we are fighting a war against an enemy seems anachronistic – we will find a way to live with it and to adapt and carry on with our lives. At the time of writing there are still a dozen or so vaccines in advanced trials, on top of the three or four already approved or moving towards approval, which is a hugely encouraging development.

We will all be delighted when we are approaching the end of repeated lockdowns, when we hear of vaccine efficacy in the older population, when we can be with our family and friends and, even better, when there is evidence that the transmission of the disease has halted.

Short of this, I suspect the virus will continue to be with us, and we will get used to a certain mortality effect on the older population, albeit to a much lesser degree than in the current year.

Trump

After four years of combative, protectionist, unilateral action, Biden is likely to be collaborative, calm and probably a more boring President. However, he will be no less determined to prevent China from benefitting from what the USA see as unfair activity, and probably no easier to deal with as the UK looks towards a new trade deal.

Brexit

Gosh, what a mess this has all become! I suspect that compared to the virus, the impact on the economy of the UK and EU will be modest, and on a global scale hardly important at all. It is a shame that the Government is less than honest in their language, as is the fact we are in this last gasp saloon. But despite all of the nonsense, the added layers of administration, some degree of travel inconvenience and so on, it will not be the end of the world and both sides will adapt accordingly. Perhaps the most likely outcome of current discussion will be what is in effect a further extension, with a deal agreed in principle, but with detail to follow in the months and years ahead.

Debt

Once again, we end the year with the most monumental build-up of debt, predominantly in the public sector for the obvious reasons of supporting livelihoods and business which lockdown would otherwise have destroyed.

Additional debt in the UK will be some £400 billion. But that is small compared to what is happening in the US where the latest, much reduced support, is a mere three quarters of a trillion dollars! This is affordable now, but not if the increase continues year on year, and easy to set to one side in the face of more urgent issues.

We can all look forward to higher taxes in the future but let us hope the chancellor takes no action that would further damage the economy as we rebuild. We could, and perhaps should, consider redistributive action as a means of reducing inequality and preventing blood on the streets, but drawing money out through tax to pay off a currently affordable debt very slowly is unlikely to help in the long run.

The idea is to grow the economy, thus shrinking the debt as a proportion of overall wealth and making it affordable for the future. Perhaps the debt will never get paid off – so long as interest payments are serviced, does it matter? Perpetuities are not new, think of war bonds.

Inflation

This is, perhaps, one of the bigger issues. You have probably seen an increase in food prices, and will do so again after 1st January. Too much money chasing limited goods will push prices up, as it has done in the past. This might be through rising investment asset prices as we saw after the 2009 crash.

This time we have printed the most enormous pile of cash and with luck this will go towards new industry opportunities and maybe it will be a means of ensuring a decent income for all, especially

if the shift to AI does hollow out middle employment opportunities (although I suspect this shift will create untold and unforeseen opportunities as it does).

So, inflation is an issue, but not an immediate one.

Conclusion

The pressure and forced changes upon society are going to lead to quicker change than otherwise would have been the case.

This change is needed but as during the industrial revolution there will be trauma, upset and, I imagine, poverty before things get better.

Huge financial opportunities will come from the changing social desires and investment and, just maybe, we will end up valuing happiness and service to others at least as much as the amount of money one has in the bank!

We have received a large number of Christmas cards again this year, which we greatly appreciate. Due to the fact that our staff are all working from home, and the logistics involved, we have decided that it would be better to make a donation to St Catherine’s Hospice this year for the amazing work they continue to do in difficult circumstances rather than send cards, which I hope you understand.

Finally, for all the trials, remember that the UK is still one of the best countries in the world in which to live, and unlike many billions of people around the world, will have a voice in and benefit from the future as it unfolds.

We sign off from 2020 with a huge thank you to you all for your ongoing support.

We wish you and your families a happy and healthy Christmas and we look forward to 2021!

Nick Matthews and the KMG Team