Investment Bulletin

A guide to blockchains

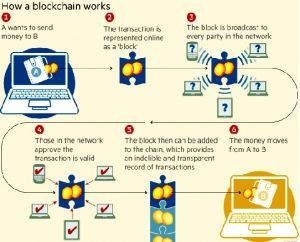

What is a blockchain?

A blockchain is a new technology for processing financial transactions without the need for intermediaries. Each transaction is encrypted into a ‘Block’ that is linked together into a ‘Chain’ using algorithms, thus creating a real-time, secure and unchangeable history of electronic transactions made.

Blockchains were first used by on-line or digital currencies, such as Bitcoin, and are now being explored by the financial services industry where Blockchains could be used initially by pension funds to improve the speed, transparency and cost of financial transactions.

This new technology has yet to overcome its teething problems, but as Bill Gates said: “We always over-estimate the change that will occur in the next two years, but under-estimate the change that will occur in the next ten. Don’t let yourself be lulled into inaction.”

What is Bitcoin?

Created in 2009, Bitcoin is a digital currency and payment system where transactions are made with no middle men, i.e. no banks. This digital currency, also known as cryptocurrency, is not issued or controlled by any government and means that you can make anonymous and instant transactions online. However, although the transaction is anonymous, it is recorded as a public record and this is what is known as the blockchain.

A new blockchain is generated around every ten minutes and is shared throughout the network which means that it constantly grows when blocks are added to the public ledger. There are countless numbers of blocks on the blockchain at any one time.

Governments could essentially lose control unless they embrace Bitcoin or similar blockchains because the likely scenario will be that blockchains will be global. This means an intrinsic linking of one currency, one tax system and one trading platform – in effect creating one world trading organisation; and the rest could be history (EU, USA, EM etc).

Some perceivable advantages are:

- preventing censorship and manipulation

- difficult to defraud

- only pay in what you want, in effect, making governments irrelevant.

The UK government is far advanced in a system called “credits”, developing it in association with the Isle of Man. A simple internet search of Ether coin will show you how to manipulate the system to run your life, and whilst there is still some uncertainty about protection and counterfeiting, it appears secure if you know what you are doing.

An example of a blockchain in use right now is in the fishing industry in Indonesia which has a complete tracking system right from when the fish are caught to when the payment reaches the fisherman, effectively allowing complete control over his or her trade. Another similar example exists in Africa with M-pessa.

There are 50 large-ish blockchains so far possibly leading to a decrease in the power of a nation’s state. With increased anonymity and empowerment of the poor and oppressed – could blockchains ultimately lead to the collapse of banking as we know it?

Kate Greenwood

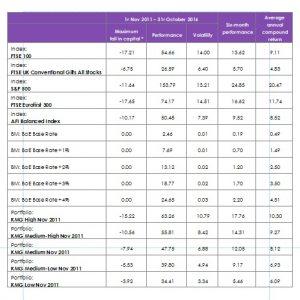

KMG performance

We are unashamed to present to you all our performance on our various model portfolios going back over five years.

Obviously, each one of you has a slightly unique overall performance depending upon when you entered the process, how we have rebalanced your affairs, and changed your risk profile etc. Please remember also performance changes depending upon whether you draw out income and/or make capital investments or withdrawals.

As you can see, however, at the end of five years, we are showing substantial investment returns.

In the table enclosed, you can see our performance against markets and our performance against our peer group.

The most important factor in our chart is the fact that our figures are quoted net of expenses, and in many cases, you have enjoyed net returns after taxation at these levels; whereas the comparative indices are before any changes and of course do not consider reductions as a consequence of taxation. In reality, therefore, our overall investment return is significantly higher than the investment return achieved by the indices against which we compare ourselves—other than of course the S&P 500!

It would have been a brave man or woman who had invested all their money into the US stock market five years’ ago and not made any changes whatsoever in that period.

The evidence that gives us and you most pleasure is lack of volatility. As you can see, your portfolio has been far less volatile than the comparative peer groups and this is testament to our rigid discipline and constant attention to detail.

We are very proud of this outcome.

Patrick McIntosh

The conundrum of risk

Risk is a daily challenge faced by financial advisers. What is risk? For each of you reading this as our client it is different. For those who attended our seminars last month you will have heard Neil Cowell from Vanguard discussing the importance of financial advisers in the role of helping you decide your appetite for risk.

Risk is defined on a Google search as “exposure (of someone or something valued) to danger, harm, or loss”. When investing, risk is about how much danger you wish to expose to your funds. The estimation of risk varies for each of us and is defined by our circumstances and experiences. For many of our clients who have been with us for many years, you have the experience of how your funds have performed over that time with some low and some high periods, but ultimately with long term growth.

Hand in hand with the investment risk you are prepared to take, is the capacity you have for loss. If the value of your funds fell in the short term, would this have a detrimental effect on your living standard? For this reason, we consider when we agree risk with you the volatility of a fund and the lowest point in recent years that it has fallen by. This helps us to manage expectations as investing should always be looked at over the long term, but of course from time to time you may need access to your funds.

So, having considered the level of risk you feel comfortable with, we then as investment managers consider a wide range of risk in the investment markets:

- political risk

- market risk or systematic risk

- inflation and interest rate risk.

Political risk is now at an all-time high with the US elections and many nationalist parties gaining traction in Europe; all of which create uncertainty for markets.

Market risk poses an interesting conundrum. Regulation has always stated that asset allocations should be a mixture of cash and fixed interest on the lower risk scale, and property then equity on the higher side of risk. But with quantitative easing on the rise and as the Bank of England uses the money it prints to buy up fixed interest funds, government stock and now corporate bonds, the government are increasing their fixed interest holdings in the process and becoming the biggest owners of their own debt and corporate debt. This has created a false market and one that is entering a dangerous balance causing an asset class that should be low risk to become high risk. Equities are running high, because with cash returns low and fixed interest not so low-risk, there is little elsewhere an investor can go to invest for some sort of reasonable return.

Inflation is now at 1%, but worryingly it takes some six months from an event for it to reflect in the figures so this increase does not yet include the effect of BREXIT and the collapse in the value of Sterling in world markets nor the increase in oil prices . It is expected that we will see a jump to 3% inflation next year. This will be a challenge to the Bank of England with little left in their tool-box to control inflation. Will we see a further rate reduction to 0.10%? We just cannot be sure of this, but we can be sure that interest rates will remain at a low level for some while simply because the level of debt in the market will have increased and the amount of debt in the system will mean a rise in rates could make a painful period for many who will struggle if the cost of their debt rises.

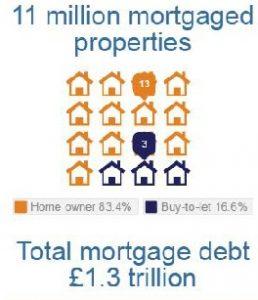

The number of mortgages as per the Council of Mortgage lenders in 2015:

This is a large amount of debt that would be challenged by rising rates! So, at KMG we continue to consider not only your personal goals and risk appetite, but the issues of all risks that come from investing!

Jenna Duffett

Who is in the driving seat… anyone?

Love it or loathe it, technology is moving faster than ever before. Just look at the content of this bulletin and the number of times we mention algorithms and blockchains and you must wonder where the human is within these processes.

We have probably all heard talk in the papers about robo-advice, and you may be forgiven for thinking the present day is turning into the 1980’s film The Terminator, but we need not be afraid of change. At KMG we are always investigating new technology and ways to streamline our processes because ultimately to us it is all about efficiency.

Where we can use technology to get information faster, more accurately and in a format that works for you, we are all for it. We do not use ‘robots’ to drive our strategy; much the same as you wouldn’t get in to a taxi and ask to go wherever it wants to take you. Our strategy is based on much more than historic data and the mathematics of the financial markets, as it is also about what is going on in the world as a whole.

The movement of robo-advice was created to fill a need. We know there are some 16 million people who fall into the advice gap, where they either cannot afford to pay for financial advice or are not interested in it. For these people the concept of being able to fill in a form with their personal details and their desired outcome and then instantly being given an answer is very appealing. But in the UK, due to our tight regulatory regime, there are concerns about the safety of electronic data and of course what is the difference between guidance and advice? Advice is of course at the heart of what we at KMG do for you. We are your holistic financial planners; we continue to guide you through budget changes, tax and generational planning and much more. But we are also forward thinkers and where we can take what we need from improvements in technology and adapt it into our processes where it is relevant to do so, we will.

As you know we look more and more to passive investments to reduce your costs and focus on the outcome that is suitable for you, and I hope you will agree that the implementation of our discretionary portfolios has already improved the speed and efficiency of rebalancing your portfolios. We are therefore already using a robot to your advantage, but ultimately we are still there, telling it what to do!

Christine Norcross