KMG’s view on the current volatility

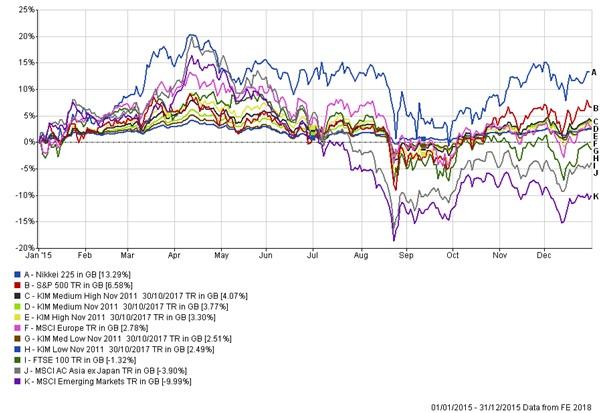

The attached graph shows the performance of KMG’s investment portfolios versus the major global markets over the last 12 months. Please bear in mind:

KMG’s performance is net of all expenses, and, to some extent for many clients, net of taxation.

The information enclosed is total return, including dividend reinvestment whether it be in KMG’s portfolios or in market indices.

The market indices are before expenses and taxation and so therefore in reality, the market performances are less than shown in the data.

Should you move into cash?

As you have moved into discretionary fund management, we can now move your investments very quickly towards cash in some or a large part of your portfolio. There are no costs in so doing, but there may be tax consequences if gains arise but, more importantly, here are the risks associated with moving into cash:

Which currency? Given sterling’s volatility as we move towards a referendum about Brexit (we saw the same in the Scottish referendum) we may find that sterling weakens dramatically during the course of this summer and therefore buying back into the market at a later date could be very expensive.

Deposit protection has fallen to £75,000 per account and therefore even though you can buy reasonably attractive interest rates by surveying the cash markets, the effort and management, time, as well as hidden costs involved in opening multiple bank accounts in order to protect your capital in the event of a banking collapse effectively means that this becomes a pretty impractical management system.

KMG, however, can manage a broadly-spread cash account. We can hold this in sterling or US dollars or euros. We can have a mixture of all three currencies. The problem is management charges. In order to spread the money effectively in order to do the necessary research to make sure the deposits we are holding will be secure, to be sure that you have liquidity and access to your money as best we can and to manage the multiple currencies that you may wish to hold, I am afraid this requires a small fee. As a consequence, if you wish to have a managed cash account, we would be delighted to do so for you, but you must recognise that:

- You will make virtually no money in terms of interest because interest rates are so small the management fees are about the same.

- You may move into negative territory as a consequence of management charges overwhelming interest earnings especially if we move to negative interest rates, ( see below)

- There is the significant possibility of currency movements against sterling.

Interest rates, in our opinion, are going nowhere for a long time to come, and we suspect that this is exacerbated by deflationary pressures.

A new type of deflation which is creating hugely volatile market performance

We are all participating in deflation; but this is not necessarily bad! What is happening is we are very, very rapidly moving to a completely new market economy. Let me highlight some extraordinary statistics:

Filling up the car, we are spending approximately a billion pounds less this year than last year. The money has to go somewhere!

Many retailers showed significant increases in festive sales earnings possibly as a consequence of significant savings in energy costs.

Aldi and Lidl are to create 150 new stores. This will equate to two billion new pounds of sales but, and here is the rub: those sales are cheaper than the equivalent sales of Tesco, Morrisons, and Waitrose, reducing prices and also profits of the old companies. Meanwhile, the profits of the new companies are likely to perform very well.

The smaller companies index in the UK last year was up 10.6% whilst the FTSE 100 as you can see by your charts was in significant negative territory.

The age of digitisation is now available to each and every one of us and enables us to become far more efficient at purchasing food, energy, and in living our lives. As we move from old industry and old ways of doing things to new ways of doing things, so the challenge for us all is to be in the right markets and not in the wrong markets. To a large extent, the headline indices reflect the old industry. We suspect we are about to spend a whole load more money on leisure activities – be it eating out, going on holiday, buying films and music.

Are we going to hell in a hand cart?

You have seen the headlines – RBS suggested everybody should move into cash, without thinking about the observations mentioned above. Some suggest the markets could fall 75% but bear in mind if this happens, then an awful lot of industries and particularly the banking and financial services industry will be in absolute turmoil such that the last place to hold your money will be in banks that will be forced into defaulting and freezing your money in those deposits.

Adair Turner, the former chairman of the Financial Services Authority has reconfirmed his view that we should simply write off the debt. You will remember that this was a question that I posed to our speakers in our autumn seminars in 2014. The fact of the matter is that at some point we suspect that the debt of developed nations will simply have to be written off because it will be too large for anybody to ever repay.

What could happen to interest rates?

We have already got negative interest rates in some parts of the world and we suspect that if the market continues to correct, the recent rise in US interest rates will go in reverse. Indeed, writing in the FT this weekend, a very sensible commentator observed that interest rates could become -5%! Yes that is right, you put in £100 on deposit, and at the end of the year, they pay you back £95. Also observed in the FT this weekend was the observation that -5% interest rates may sound completely stupid but then again if I had said to you eight years’ ago that we would have printed money out of thin air, you would have told me that that was utterly stupid and the world would simply have ceased to function. Well we have printed all the money, the world continues and we simply do not want to believe the truth!

KMG prefers to remain fully invested

May I remind you from our autumn seminar, of the slide which is again attached which shows that being out of the market on critical days destroys wealth. In our opinion, we cannot afford to be out of the market because whilst we cannot time the top, we also cannot time the bottom and we must stick to fundamentals. Holding cash means that you stand still and will not see the upside when markets bounce back.

The digital world and energy prices are driving down the price of absolutely everything yet wages are stable and economic activity continues – companies are doing reasonably well. There is a vast amount more money in circulation whether you are in developed economies or in emerging nations. Even if you are simply living on a dollar a day which the vast amount of the global population are still doing, the fact that energy prices have come down means that even these people now have more opportunity to improve the quality of their lives. This drives global growth, activity and expansion.

The price of energy drives down the cost of absolutely everything – food, clothes, transportation, pharmaceutical products –lower energy costs are far more beneficially than interest rate cuts or tax cuts. Energy prices are really what drives the expansion of the global economy.

The digital world, the internet and all the benefits that we get from a dramatic change in the way in which we think about how we live our lives enable us to live efficiently, effectively, profitably, comfortably and this will expand the global economy. Humans are addicted to consumption. We might wish we could save more money, but in general we humans are not going to do so. We are going to consume, and as a consequence KMG will continue to concentrate on investing in the trends which will expand the global economy whilst avoiding the dinosaurs of the past and the inefficient companies currently trading.

We would prefer to maintain a very thinly-spread, globalised investment portfolio which can benefit from:

- some capital appreciation, albeit possibly very modest

- some dividend income, albeit that we recognise that these dividends may be lower than they have been in the past, and

- we wish to reduce being too exposed to any one currency and we wish to avoid being exposed to a banking collapse or a crisis of confidence in printed money.

In the end, investing in real things must be the safest way to protect your wealth and to secure your future, however volatile and unpleasant the journey may be in the short term.

Conclusion

For all the reasons set out in this bulletin, we recommend that you leave your funds fully invested in the markets. We believe that this is the best strategy for preserving your wealth through the current bout of market volatility.

What do you need to do?

If you are happy to leave things as they are, then we will be commencing a quarterly realignment of your portfolio, maintaining the same strategy but restoring the asset allocations (i.e. the proportions of equities, bonds, property and other asset classes) within your portfolio back to their original position to ensure that the risk profile of your portfolio is maintained.

You need do nothing if you wish to remain invested. We will undertake the realignment the week of 8th February providing you with the required two weeks’ notice of trading activity on your portfolio.

If you wish to move into cash for some or all of your portfolio, you need to send us an instruction to do so, (preferably by email), or alternatively by telephone.

Please remember that under the discretionary fund management system, we do not need signed pieces of paper from you, and we can therefore move quickly, efficiently and effectively once you have contacted us.

We would be delighted to talk with you regarding this note and your affairs and to provide further reassurance, so please do not hesitate to contact us if you wish to do so.

Patrick McIntosh

18/1/16